大智若愚 -- The great wisdom may seem dumb.

大道至简 -- The ultimate sophistication is simplicity.

When investing, people tend to think of buying and selling. For each trade, they have to answer at least 3 questions correctly in order to make profit:

Such trading mentality could be harmful to investing. I would argue that the most important investing decision is actually "How long should I hold my investment?" Once the issue gets resolved, the rest of investment questions become secondary and can be answered easily.

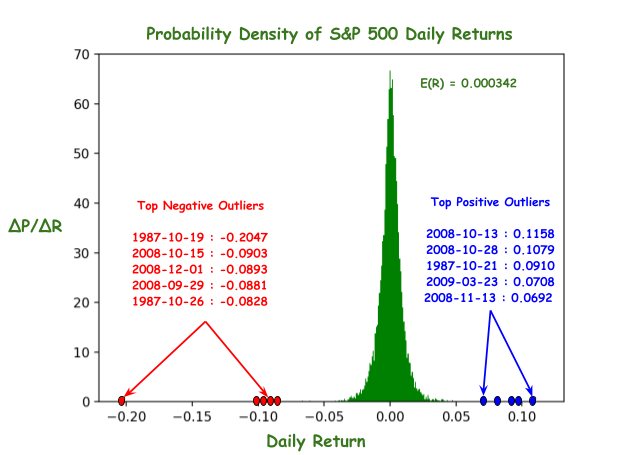

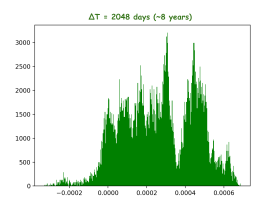

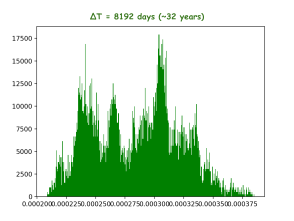

To see why, let's look at the Probability Density Function (PDF) of S&P 500 daily returns for the holding period of one trading day:

The probability distribution of returns seem pretty random. People may say the market's efficient because it's very hard for anyone to consistently pick positive days and avoid negative days. If we increase holding periods (in trading days), the expected normalized daily returns (geometric mean) don't change too much but the shapes of the corresponding PDFs change significantly:

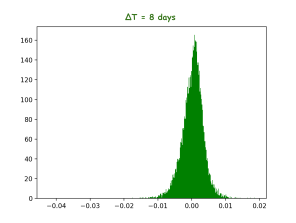

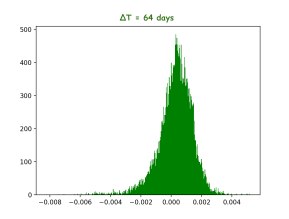

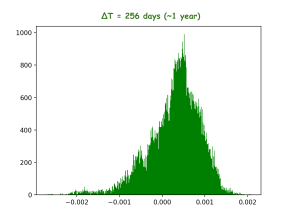

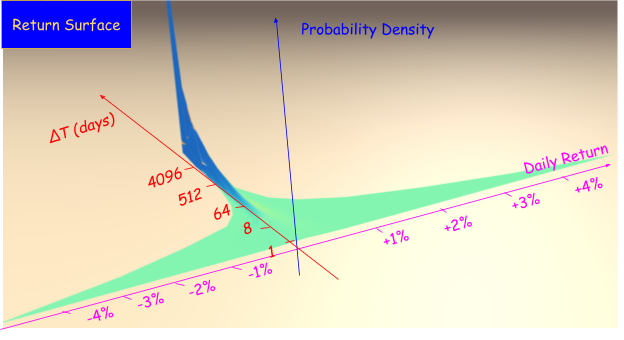

If we put all PDFs across all holding periods (delta T) together, we get a return surface showing how normalized daily return's distributed: it spreads over a wide range of positive and negative values when holding periods are short, and the distribution becomes very concentrated when holding periods are long. If holding periods are longer than 10 years, you're almost certain to get non-negative returns.

If we put all PDFs across all holding periods (delta T) together, we get a return surface showing how normalized daily return's distributed: it spreads over a wide range of positive and negative values when holding periods are short, and the distribution becomes very concentrated when holding periods are long. If holding periods are longer than 10 years, you're almost certain to get non-negative returns.

An average investor has10,000~15,000 (trading) days to act. If we represent it by a line of 10,000~15,000 day long, what investors do in their lifetime is to break the line into small pieces and place them onto the return surface. A successful life-long investment is to put more pieces on the positive side than negative side. At the first glance of equity return surface, it should be immediately obvious why long term indexing makes sense. No modern financial theories or complex arguments are required to see the insight.

It's hard to identify good stocks, and it's even harder to time the market. I don't believe that I have any inherent advantages over other market participants. I doubt my ability to identify good investments and make profitable trades consistently. I know my mind will degrade due to aging and my experience may become less relevant due to unforeseeable paradigm shifts. In a word, the more investment decisions I have to make, the more likely the distribution of my investments will spread on the return surface randomly.

Therefore, my investment strategy shall NOT depend on my ability of being an outliner. To ensure all my investments stay on the positive side on the return surface is to make as few decisions as possible. The single most important investment decision I'll make is to decide the holding periods of my investments. If my holding periods are very long (forever), it almost guarantees that my investments will always yield positively, actually historical data suggests close to 100% if holding periods are > 20 yrs.

If returns are always positive, leverage will magnify them in my favor. It's just simple math, no complex concepts or fancy theories. So, the second investment decision I'll make is the leverage.

Once I decide that I should hold my investment forever (forever ~= lifetime), I can settle the 3 trading questions once for all:

In summary, my investment is guided by Principle of Least Actions:-) minimize the number of decisions I have to make for my lifetime. The only trick I will use to beat the market is leverage, nothing else. To translate the principle into everyday practice, I will:

Based on historical S&P data, people born around 1930s, e.g. Warren Buffet, only need to correctly adjust leverage ratios 2 or 3 times to beat Warren Buffet. In another word, if we have 8 monkeys and instruct them to toss a fair coin to adjust leverages once every 10~20 years, there will be one monkey who can beat or match Warren Buffet and his Superinvestors of Graham-and-Doddsville. If the monkeys don't bother to become legendary investors, they just need to maintain a constant leverage and easily beat the market for doing nothing*.

- What to buy?

- When to buy?

- When to sell?

Such trading mentality could be harmful to investing. I would argue that the most important investing decision is actually "How long should I hold my investment?" Once the issue gets resolved, the rest of investment questions become secondary and can be answered easily.

To see why, let's look at the Probability Density Function (PDF) of S&P 500 daily returns for the holding period of one trading day:

The probability distribution of returns seem pretty random. People may say the market's efficient because it's very hard for anyone to consistently pick positive days and avoid negative days. If we increase holding periods (in trading days), the expected normalized daily returns (geometric mean) don't change too much but the shapes of the corresponding PDFs change significantly:

It's hard to identify good stocks, and it's even harder to time the market. I don't believe that I have any inherent advantages over other market participants. I doubt my ability to identify good investments and make profitable trades consistently. I know my mind will degrade due to aging and my experience may become less relevant due to unforeseeable paradigm shifts. In a word, the more investment decisions I have to make, the more likely the distribution of my investments will spread on the return surface randomly.

Therefore, my investment strategy shall NOT depend on my ability of being an outliner. To ensure all my investments stay on the positive side on the return surface is to make as few decisions as possible. The single most important investment decision I'll make is to decide the holding periods of my investments. If my holding periods are very long (forever), it almost guarantees that my investments will always yield positively, actually historical data suggests close to 100% if holding periods are > 20 yrs.

If returns are always positive, leverage will magnify them in my favor. It's just simple math, no complex concepts or fancy theories. So, the second investment decision I'll make is the leverage.

Once I decide that I should hold my investment forever (forever ~= lifetime), I can settle the 3 trading questions once for all:

- What to buy? -> The Market - Because it's the only investment vehicle that may last for my lifetime.

- When to buy? -> Whenever I have cash available for investing.

- When to sell? -> Never.

In summary, my investment is guided by Principle of Least Actions:-) minimize the number of decisions I have to make for my lifetime. The only trick I will use to beat the market is leverage, nothing else. To translate the principle into everyday practice, I will:

- Keep buying broad-based index ETFs/funds tracking productive assets such as S&P 500 and hold them forever.

- Control one and only one parameter, leverage ratio. Roughly speaking, 2~3x when I'm young and ~1 when my salary no longer matters. I may go beyond the range under extreme market conditions, e.g. market crashes or melt-ups. But, extreme conditions don't happen often and I shall make no more than 2~3 leverage change decisions for my whole lifetime. I already made one in May 2009, so I have at most 2 major leverage decisions left.

- Live modestly relative to my net worth. For example, consume no more than 1~2% of my investment (~ dividends of S&P 500). Find a job to cover the cost and/or lower my living expense if the returns on investment are not enough to sustain my current lifestyle. Retire when my W2 no longer makes difference.

S&P 500 Relatively Returns

S&P 500 Accumulative Returns (1950 == 1)

* A monkey's born in the same year as Warren Buffet can outperform the market for each and every day since 1950 if he maintains a constant leverage.

* Rule #3 is key to survive downturns like 1975, 1987, 2001, and 2009.

The empirical data and simple math may be assuring to someone, but there simply aren't enough historical data to prove anything+. Therefore, the hardest part to implement this strategy is the capacity to do nothing: I have to resist the temptation to react to day-to-day events. I have to live in a world full of fear, doubt, and uncertainty, and commit to something long before I can see the final result.

* Maintaining a constant leverage ratio could be viewed as an extension of Kelly Criterion, a strategy trying to maximize accumulated return while avoiding gambler's ruin. The following book gives a detailed discussion on the relevant theories and practices:

記得有研究顯示,最好不要超過2倍

ReplyDeletenice post and explanation.

ReplyDeletejust wondering if you have changed your strategy during this current melt-up since covid crash.