From January 1980 to August 1995, the stock market experienced a phenomenal run. The S&P 500 delivered a total return of approximately +833% (including dividends reinvested), corresponding to a compound annual growth rate (CAGR) of roughly 15–16% over this 15–16 year period. Since its inception in 1926, the S&P 500 has averaged about 10.4% annualized return, making it reasonable to expect some mean reversion in the years that followed.

However, when Netscape IPO debuted on August 9, 1995, its stock price leaped from $28 to $75, marking a pivotal moment that ignited investor enthusiasm for internet companies. Over the next 333 trading days, the S&P 500 gained an additional ~30%.

On December 5, 1996, then-Federal Reserve Chairman Alan Greenspan famously described the market euphoria as “irrational exuberance”. The Tokyo market, open during the televised speech, immediately fell and closed down by 3%, with markets worldwide following suit. Yet the correction proved short-lived: the S&P 500 continued to surge for another 3.3 years, ultimately peaking in March 2000, averaging a CAGR of roughly 26% after the Greenspan speech.

The 2000–2002 bear market, triggered by the bursting of the dot-com bubble, was exacerbated by the terrorist attacks on September 11, 2001. The S&P 500 bottomed out around 776 on October 9, 2002. From its March 2000 peak (~1,527), the index lost roughly 49% of its value. The Nasdaq-100 index, heavily weighted toward technology stocks, fell even more dramatically to 815—an approximate 82% decline from the peak (~4,700).

It took the S&P 500 roughly five years to climb back to 1,565 by October 2007, before plunging again to 676 on March 9, 2009, a level the index had first reached as early as July 1996.

Following this low, the S&P 500 entered a prolonged bull run, averaging a CAGR of 16~17% over the next 16 years. The tech-heavy Nasdaq-100 Index, the major growth driver of S&P 500, achieved an even higher CAGR of roughly 20~21%. As of August 21, 2025, the Nasdaq-100 has a total market capitalization of ~$30 trillion, accounting for about 60% of the S&P 500’s total market cap (~$57 trillion).

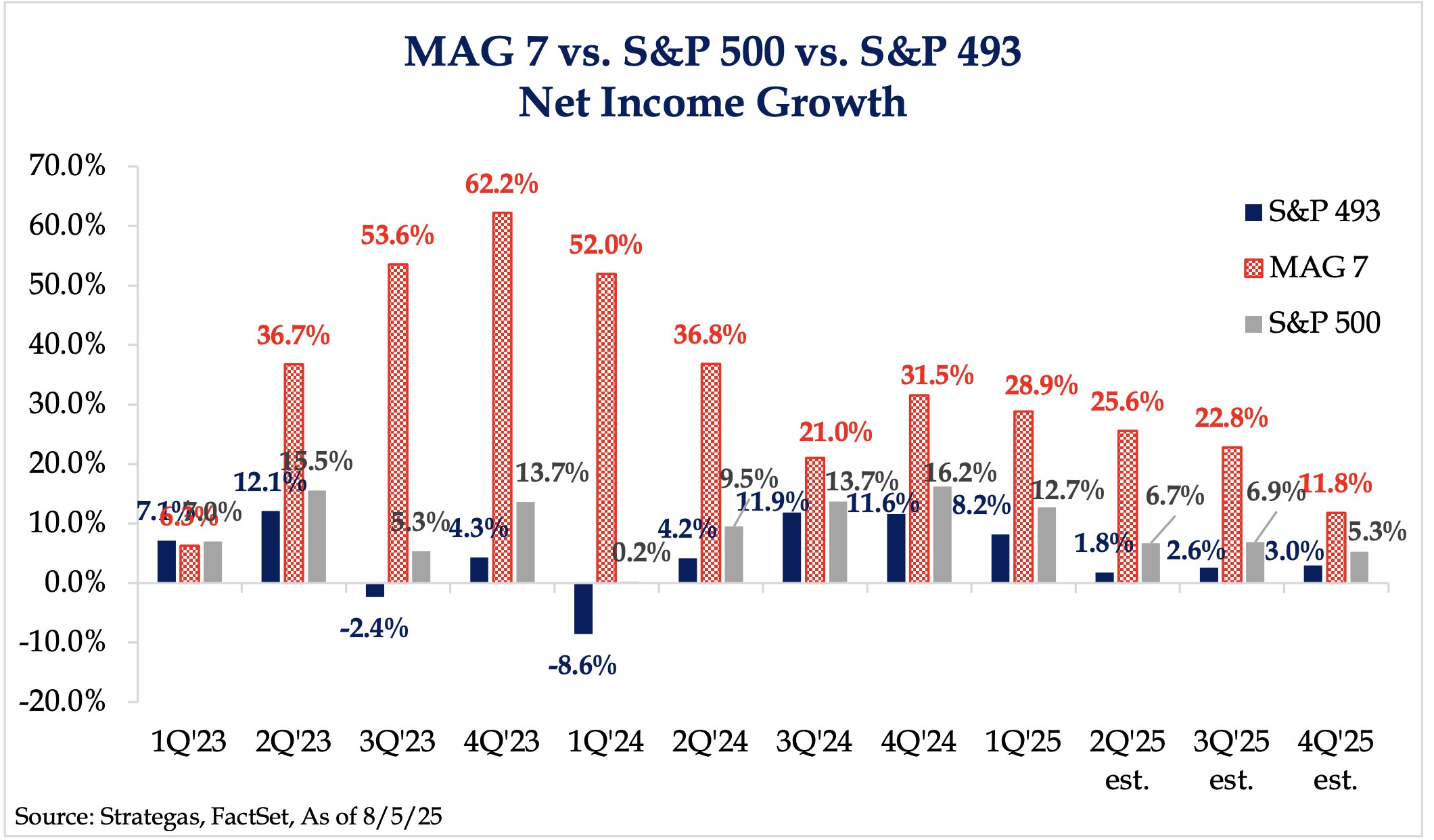

The release of ChatGPT on November 30, 2022 was an event as transformative as Netscape’s IPO was for the Internet era, marking the beginning of a new AI era.

Over the past 2.5 years, an AI bubble has clearly been forming: valuations of AI startups and compensation for top AI engineers have soared to levels that would have seemed unimaginable just five years ago

Suppose the unfolding of this AI bubble follows the timeline of the dot-com bubble, and someone as prominent as Alan Greenspan warns that the current market euphoria is irrational exuberance. How would you invest?

Are you going to act on the irrational exuberance that will burst in 2~3 years, or the rational exuberance that will be realized in 20~30 years?

If you're concerned with a near-term crash, is it realistic for you to stay out of the market for ~6 years (as in Oct 2002) or ~13 years (as in Oct 2007)?

Even if you have the foresight and patience, how would you determine the right moment to re-enter the market without missing a long bull run, like the one from 2009 to today?

==================p.s. Zuck on AI CapEx bubble

https://x.com/The_AI_Investor/status/1969042538976751937

pp.s. AI CapEx and Revenue